Why Does a $100K Salary Feel Like You're Only Making $50K? (And What High-Earning W2 Employees Are Doing About It)

The tax-advantaged pension structure that business owners have used for decades—and why most W2 employees don't know they qualify:

Watch this video first:

About Madison

Madison didn't start out as a financial strategist—she started as someone who felt the tax system was rigged against working families.

Years ago, while her ex-husband worked on oil rigs for weeks at a time, Madison was home with two young kids, managing a household on one income.

Despite earning well over six figures, nearly half of it disappeared to taxes before they ever saw it.

"I watched us pay more to the government than we spent on our mortgage, childcare, and groceries combined," she says.

"And when I asked our CPA what we could do about it, he just shrugged and said 'that's how it works.'"

That wasn't good enough.

Madison started researching.

She discovered that business owners, professional athletes, and Fortune 500 companies had been using advanced pension structures for decades—strategies her CPA had never mentioned.

Not because they were hiding them, but because most accountants simply don't specialize in proactive tax planning.

She implemented these strategies for her own family, then earned her credentials to help others do the same.

Today, Madison works alongside her father, who brings 40 years of experience implementing pension and wealth strategies for farmers, business owners, and high-income professionals.

Together, they've helped hundreds of clients stop overpaying and start building protected wealth.

Madison holds a bachelor's degree and operates within CFP®-aligned planning standards. But what she's most proud of is this:

she's lived the frustration her clients feel, and she knows exactly how to fix it.

"I'm not here to sell you something you don't need.

I'm here to show you what's been available all along—and make sure you don't leave money on the table like I almost did."

Why Your CPA Hasn't Told you About This

If you're like most high-earning W2 employees, you trust your CPA to handle your taxes.

And they probably do a great job—filing your returns, keeping you compliant, making sure the numbers add up.

But here's what we've learned after working with hundreds of clients:

Most CPAs are trained in tax compliance, not proactive tax planning.

They're excellent at making sure you don't mess up.

But they're not equipped to design advanced strategies like pension structures, trust integration, or tax-advantaged insurance planning.

It's not that they're hiding anything from you.

It's simply outside their expertise.

Here's Exactly What You Get On Your Strategy Call:

If you're making $150K+ as a W2 employee, you're likely losing $25K-$40K to taxes every year. That's $125K-$200K over 5 years—enough to buy a business, fund early retirement, or build generational wealth.

That's not a tax problem. That's a structure problem.

Business owners making the same income keep significantly more—not because they cheat, but because the tax code rewards business structures differently than W2 income.

Since 2006, those same structures have been available to W2 employees with side businesses. Most people just don't know about them.

On this complimentary strategy consultation, you'll learn:

1. Where your money is actually going (federal, state, FICA—we'll break down your current allocation so you can see the reality)

2. The pension framework used by the NFL, Fortune 500 companies, and government agencies (and why small business owners got access in 2006)

3. Whether you're a candidate based on your income, business plans, and financial goals (not everyone qualifies, and we'll tell you either way)

4. Your implementation timeline if you decide to move forward (including which professionals you'll need and what the process looks like)

This is education, not persuasion. I'm going to show you the numbers and the structure. You'll decide if it makes sense for your situation.

The only thing at risk is staying where you are.

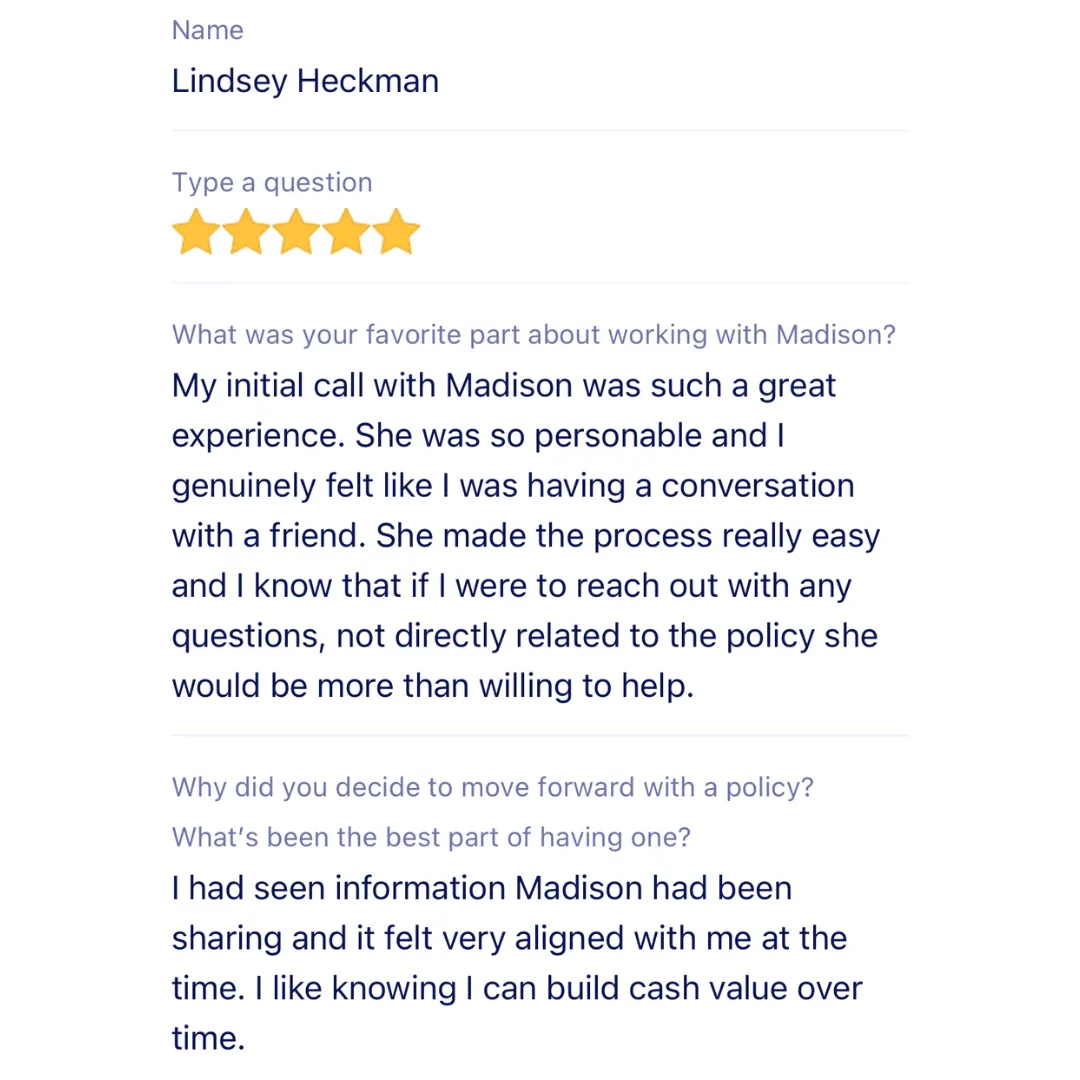

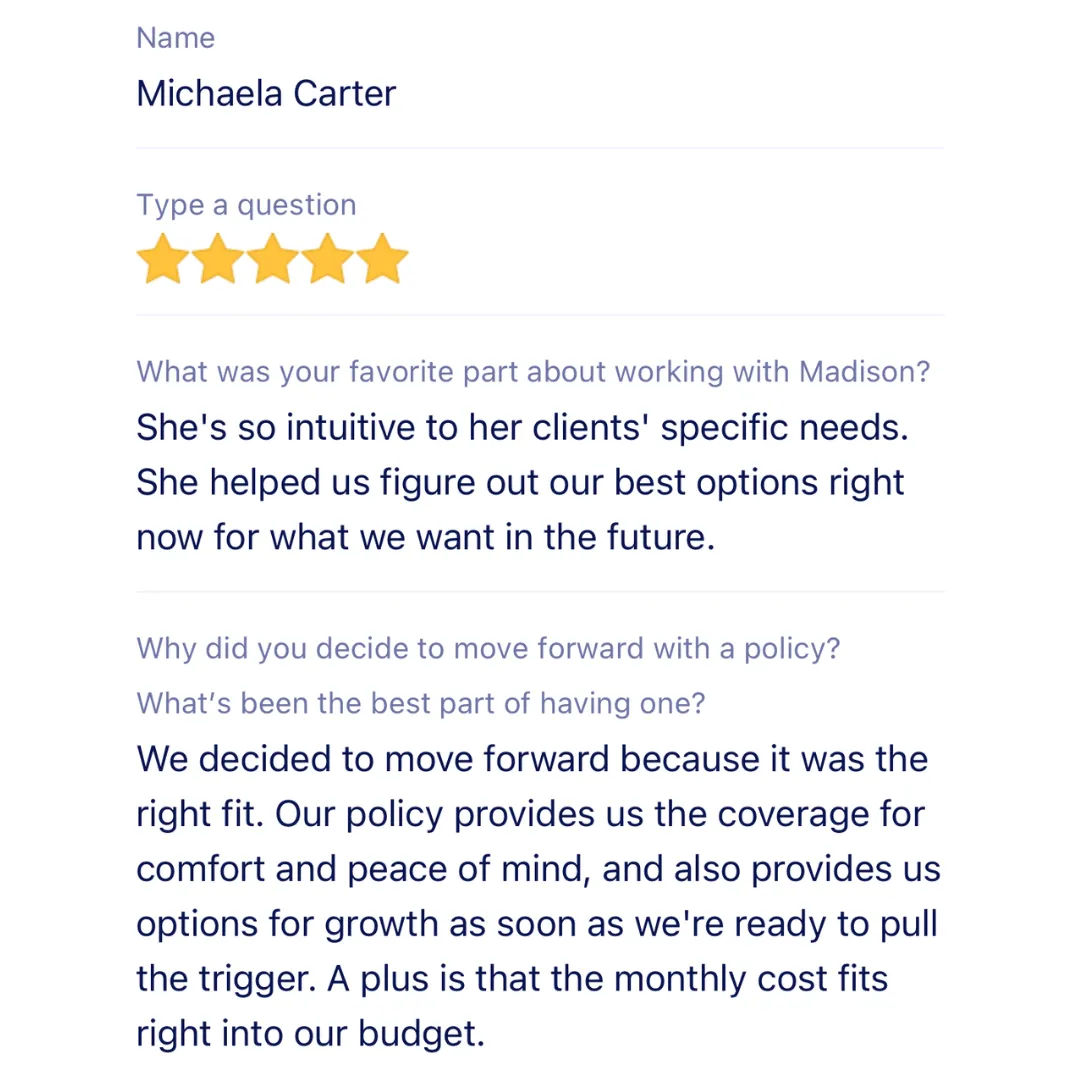

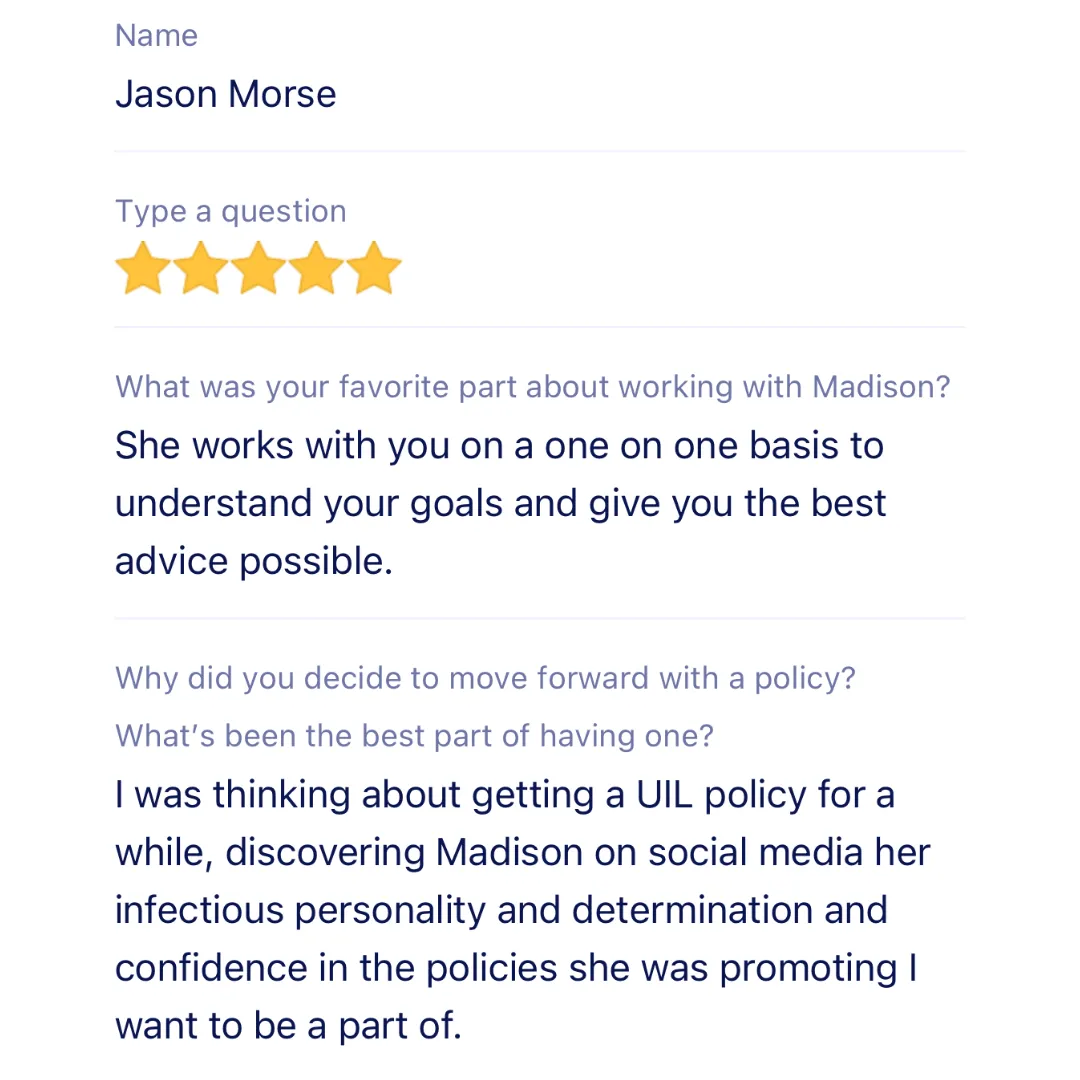

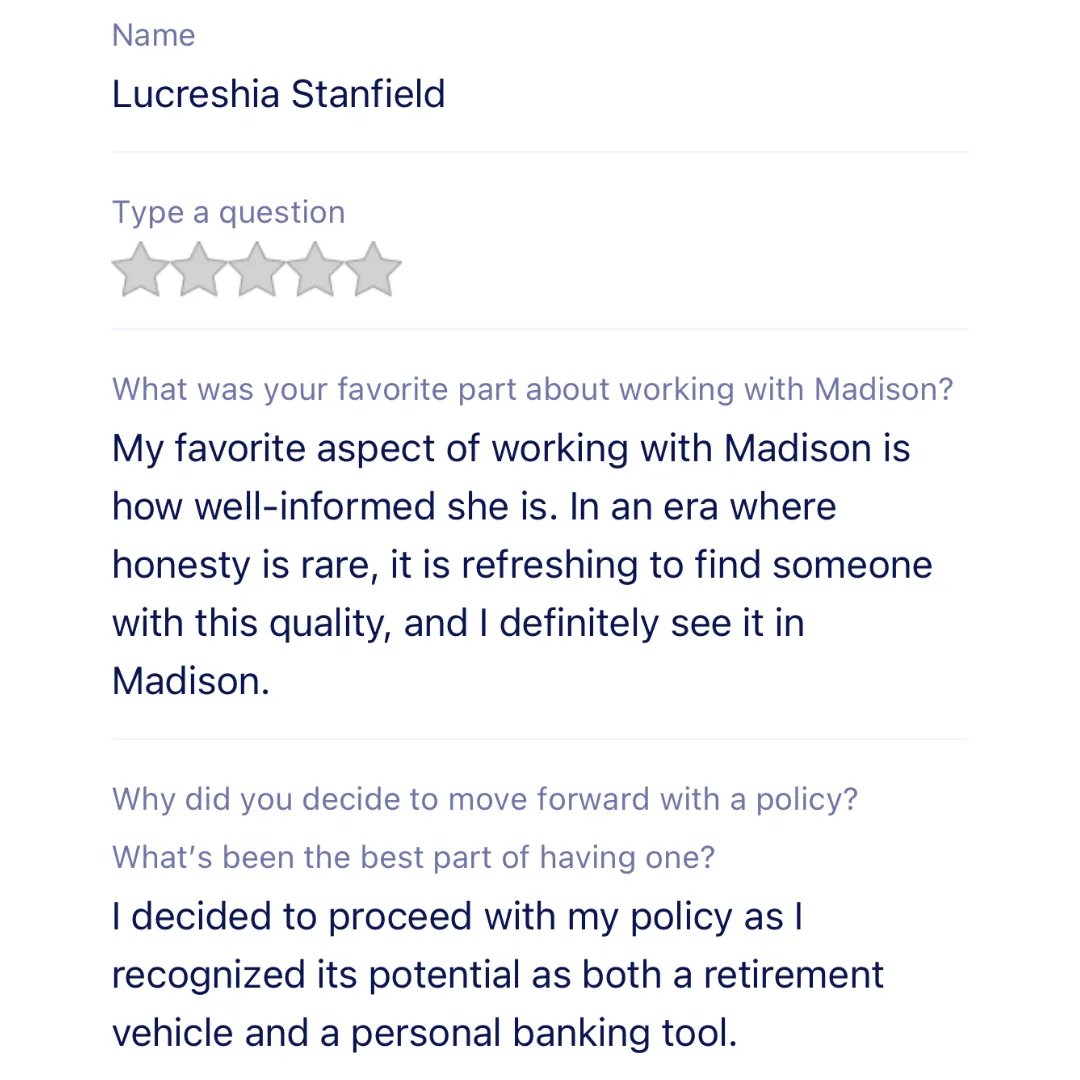

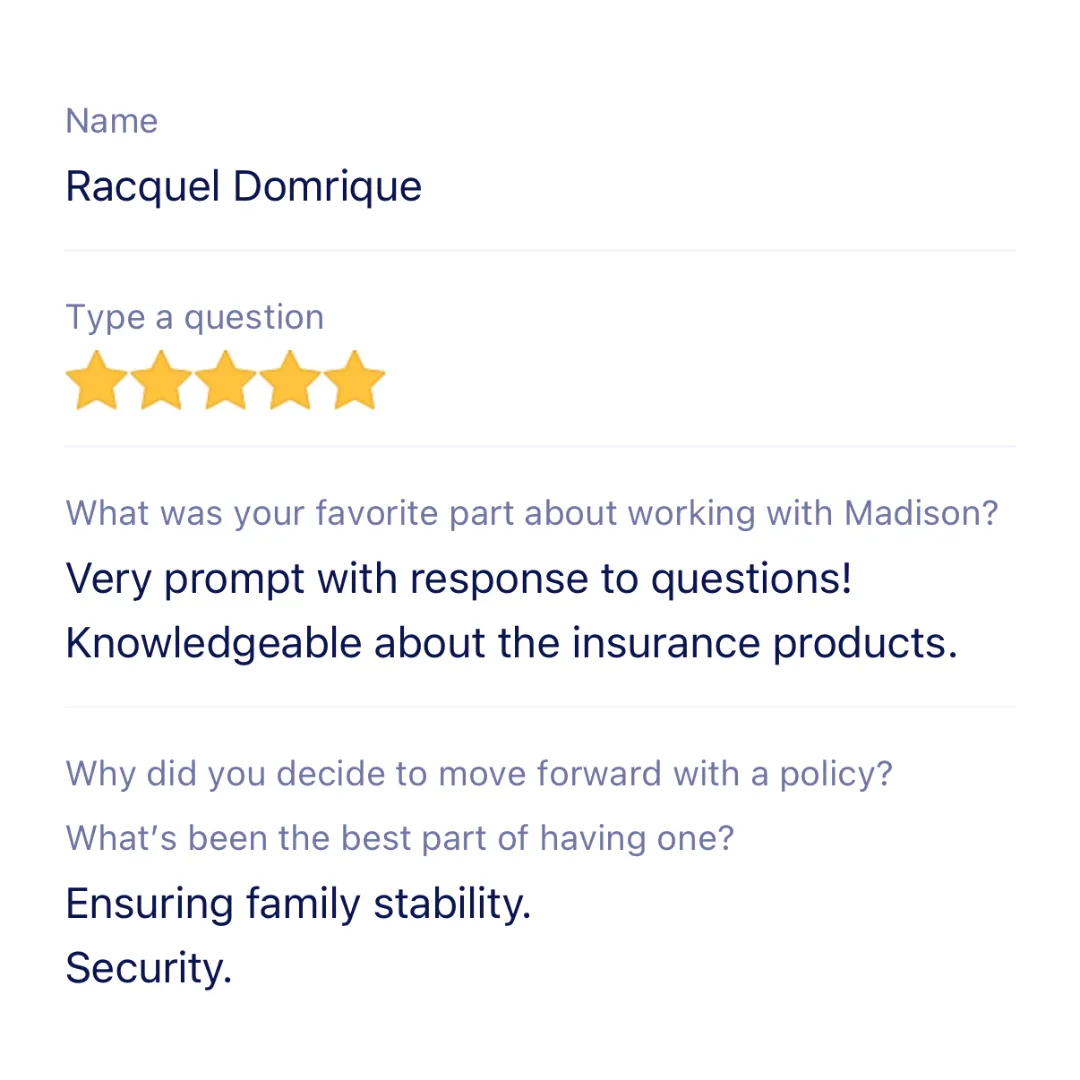

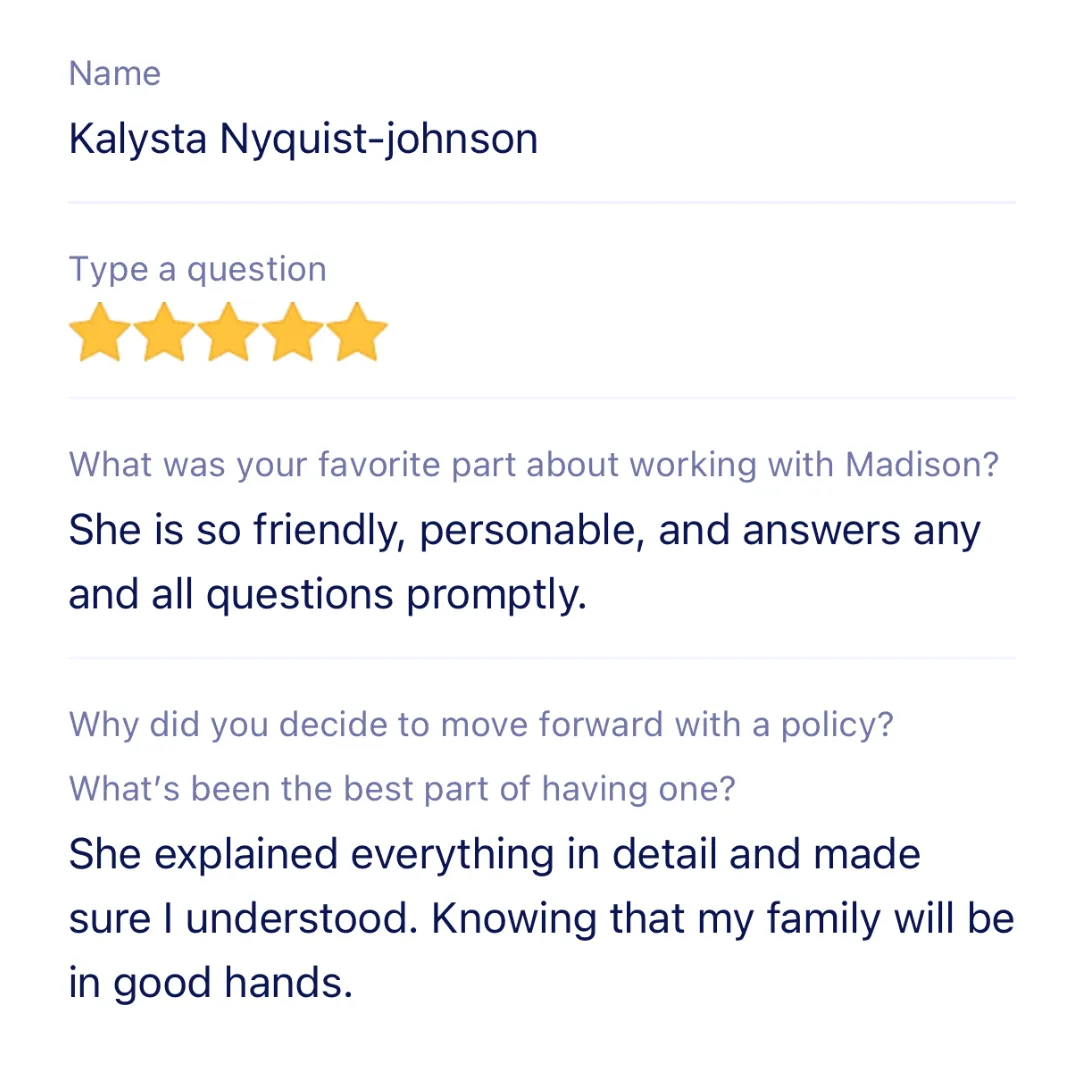

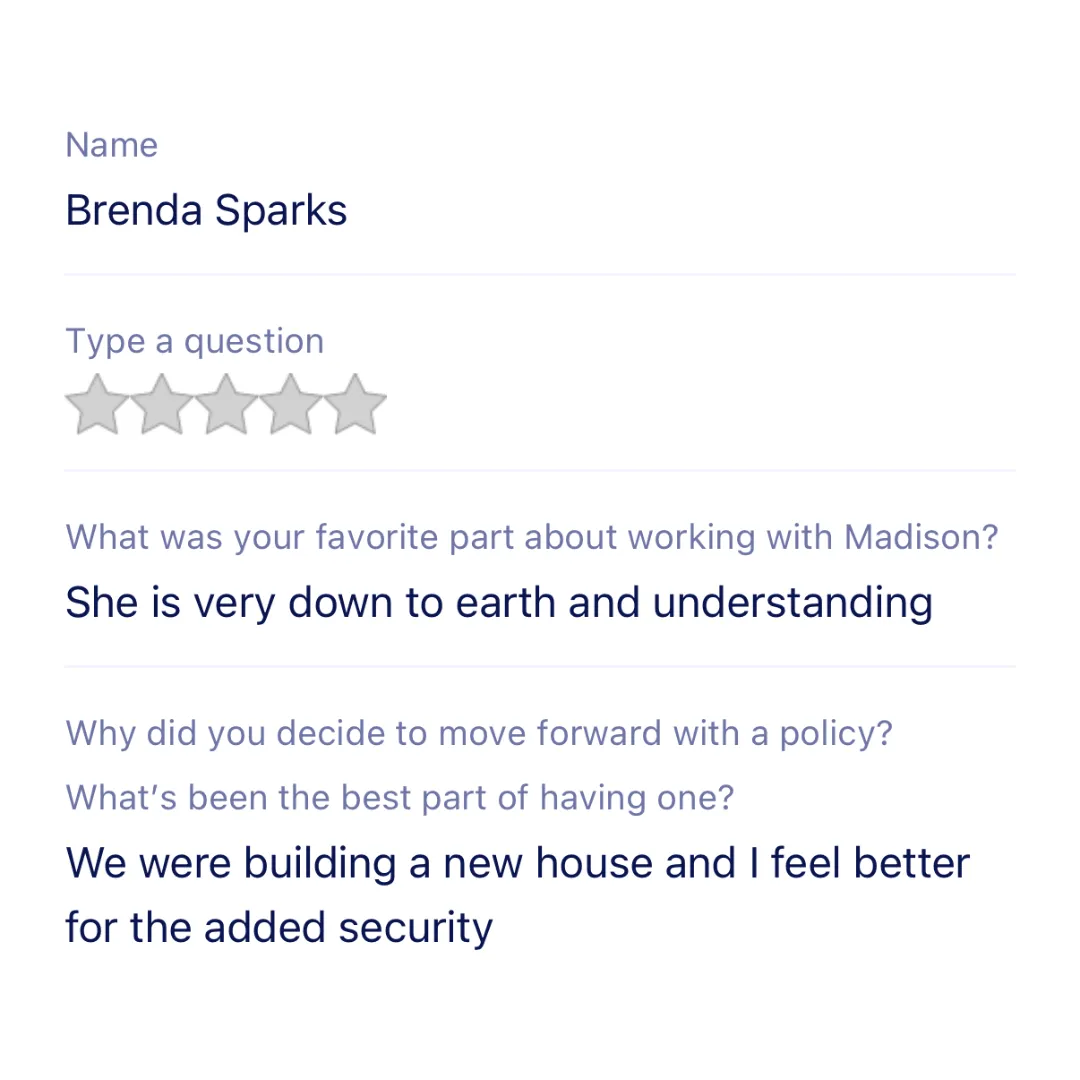

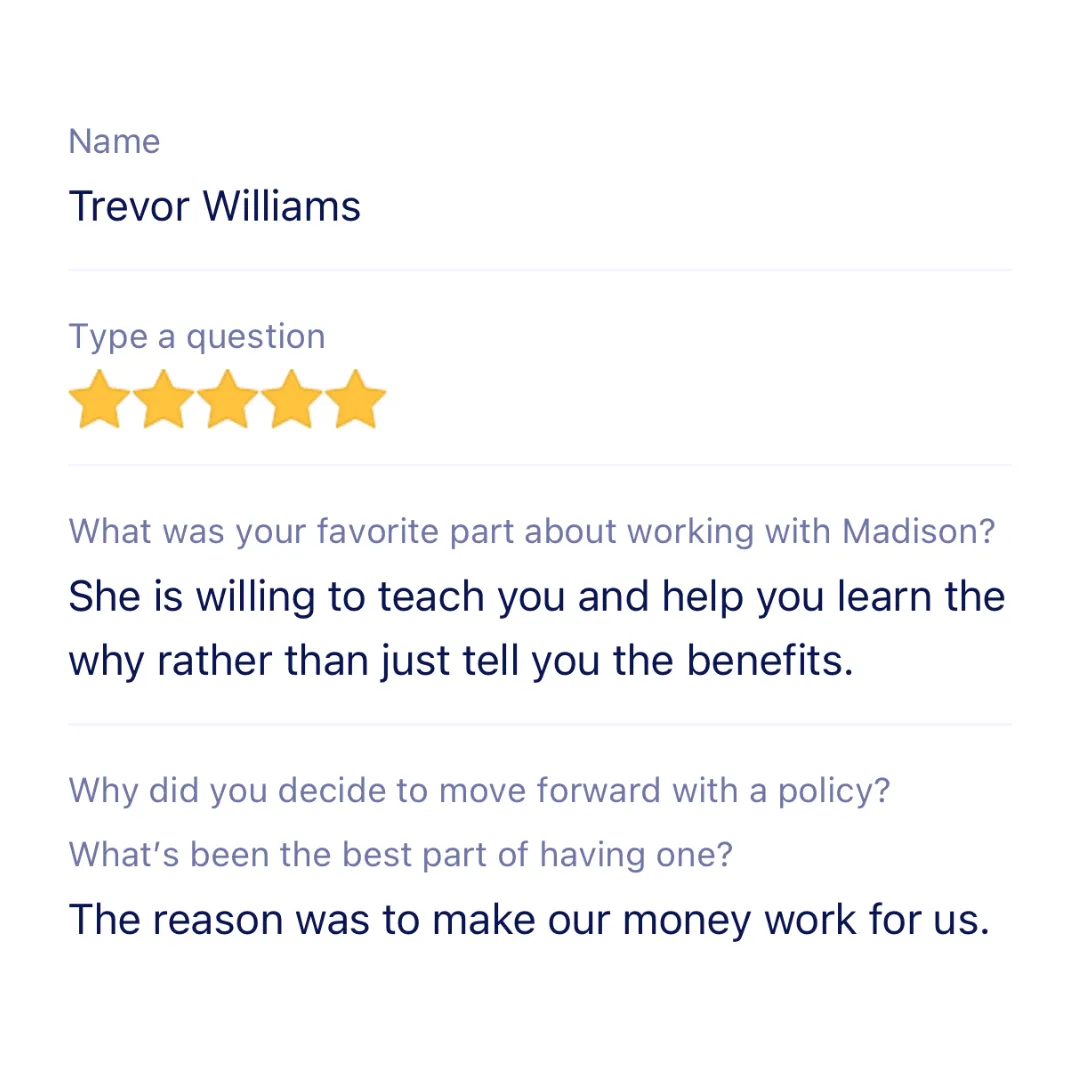

What People Are Saying

Book a Call

IMPORTANT NOTE: Madison provides financial strategy education and planning. She works alongside a team with over 40 years of collective experience. All strategies discussed should be reviewed with your personal CPA, tax attorney, or certified financial professional before implementation. We do not provide tax, legal, or investment advice.